Company is in the business of designing, manufacturing, branding and selling of ready-made apparels in the men’s segment and other accessories under various brands. Company brands range from the high fashion premium segment such as ‘Killer’ for denim wear and ‘Easies’ for casual wear to the middle and economy segments through brands such as ‘Lawman’ and ‘Integriti, DESI BELLE for woman wear and Addictions for accessories division.

Company’s manufacturing plants are at: – 1. Dadar (Mumbai) 2. Goregaon (Mumbai) 3. Vapi (Gujarat) 4. Daman (Union Territory)

Company has total annual capacity of 4 million pieces.

This is the main strength of the company as it is fully integrated company starting designing to stitching to sales as in this way they will utilize their inventory more efficiently and hence good control over the cost and according to me this is the main reason that company never post loss since its IPO in 2006 as in between 2006 to 2023 company faces the financial crisis of 2008 as well as coronavirus of 2020.

Company’s distribution channels are: – 1. Company own store (K-Lounge) 2. Large Format Stores (LFS) like Reliance Retail, Max Lifestyle, Shoppers stop and others 3. Multi Brand Outlets (MBO) 4. Exclusive Brand Outlets (EBOs) 5. E-Commerce and 6. Exports.

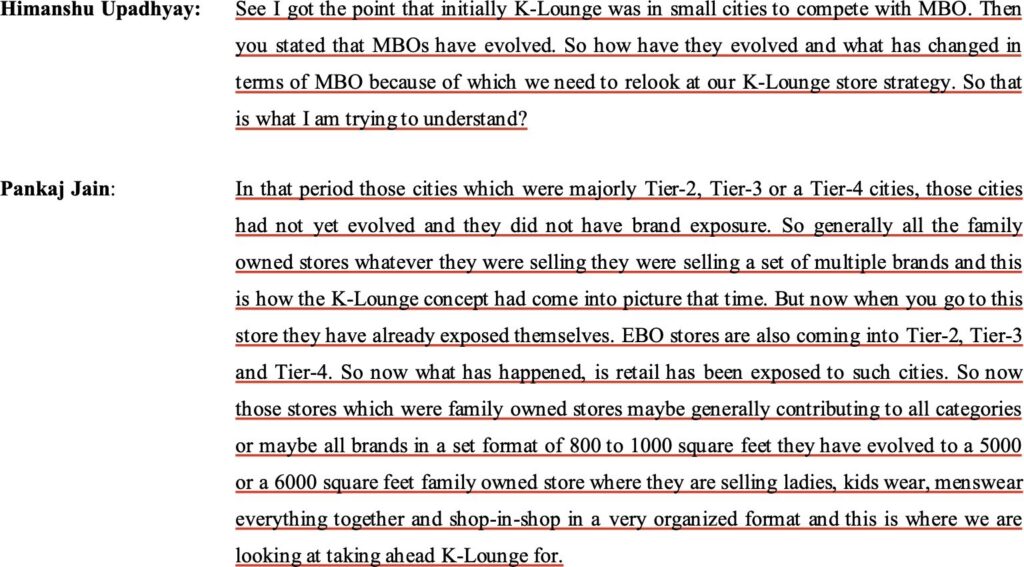

Earlier company focusses more on K-Lounge store where they sell all their brands but from past one year company has changed their policy and converted aggressively K-Lounge store mostly into Killer store or their other brand store exclusively, in recent January 2024 concall one participant ask the reasons for the same and below is the reason which company gave

So basically according to this conversation due to the size of the store company is planning to convert existing K-Lounge store into exclusive brand store and in future they will open the K-Lounge in large size store.

Company Brands:

Killer

The Company’s flagship brand Killer imbibes in it the cool confidence of today’s youth and redefines denims, giving a bold character to them. Killer is a powerful and iconic brand and is regarded as one of the established and well-regarded denim brands in India. Killer continues to be the flagship brand amongst our brand portfolio which contributed to more than 60% of total income from sales of apparel and lifestyle accessories.

Integriti

Reflecting and resonating the ambition and energy of youth, Integriti offers a credible, trusted and value proposition across work and casual wear and helps to offer product range to a different price segment. Integriti is the second largest brand for the Company.

Lawman Page 3

A glamorous, lifestyle brand, LawmanPg3 specialises in trendsetting denim and partywear for young adults. The brand plays a unique role in bringing the glamour quotient to the fashion wardrobe. In the last year,

the Company had signed Rohit Shetty as the brand ambassador for the Brand LawmanPg3.

Easies – By Killer

A blend of classic and contemporary preferences, Easies – By Killer is reshaping corporate fashion in India through its range of semi-formal menswear, made from the most premium range of fabric and linen. Easies

a well-established brand known for its collection of chinos, shirts and has a dedicated customer following supported by the increasing trend of semi-formal wear.

Desi Belle

Desi Belle, the emerging brand amongst our portfolio is an Indo-Western womenswear focused brand that exists at the confluence of modern style and desi touch, catering to the contemporary woman.

Product Wise sales:

Jeans: Jeans sales stood at ₹ 39,630.35 lakhs contributing to 51.19% of the total income from sales of apparel and lifestyle accessories in FY2023 as compared to ₹ 34,056.38 lakhs in the previous year contributing to 56.28% of the total income from sales of apparel and lifestyle accessories. However there has been an absolute growth in terms of value from this category, the percentage fall in revenue contribution from Denims clearly reflects the concentrated efforts of the Company to diversify its revenue streams across product categories.

Trousers: Trousers sales stood at ₹ 6,746.42 lakhs in FY2023 as compared to ₹ 4,708.73 lakhs in the previous year. Trousers contributed 8.71% of total income from sales of apparel and lifestyle accessories revenues as compared to 7.78% in the previous year.

Shirts: Shirts contribution to total income from sales of apparel and lifestyle accessories stood at 21.51% with sales of ₹ 16,651.85 lakhs in FY2023 compared to ₹ 11,082.22 lakhs in the previous year.

T-shirts: T-Shirts sales stood at ₹ 3,706.64 lakhs contributing to 4.79% of the total income from sales of apparel and lifestyle accessories from ₹ 3,025.72 lakhs in the previous year.

Company Promoters – Company Promoters have been associated with the apparel manufacturing business since 1980. Originally, two of our Promoters, Mr. Kewalchand P. Jain and Mr. Hemant P. Jain entered into apparel manufacturing business through a partnership firm called M/s. Kewal Kiran & Co. Mr. Dinesh P. Jain and Mr. Vikas P. Jain were subsequently taken as partners in M/s. Kewal Kiran & Co. in 1994. Over a period of time, Kewal Kiran group comprised of various companies and firms. It was long felt need of the promoters to consolidate the business under single corporate umbrella to achieve the benefits of consolidation of marketing and manufacturing operations. Hence, the restructuring started with the conversion of the partnership firm, M/s. Kewal Kiran & Co. into a private limited company under Chapter IX of the Companies Act on 31st July, 2002.

Kewalchand P. Jain

Chairman & Managing Director

Mr. Jain, a keen student of finance and our hands-on manager, was instrumental in introducing the branded apparel segment to KKCL. He oversees the Company’s finance functions and is responsible for the overall management of the Company’s affairs. He is also the acting Trustee of Smt. Jatnobai Karmchandji Ratanparia Chauhan Charitable Trust.

Hemant P. Jain

Joint Managing Director

Mr. Jain has played a key role in launching Killer and Easies brands. He is in charge of the Killer and Easies brands and supervises operations of the Desi Belle brand. He also oversees the retail business of the Company. He is one of the Trustees of Smt. Jatnobai Karmchandji Ratanparia Chauhan Charitable Trust.

Dinesh P. Jain Whole-time Director

Mr. Jain manages the manufacturing operations of the Company. His specialisation lies in production, human resources and industrial relations. His leadership ensures optimum utilisation of the Company’s production facilities, its personnel and overall development. He is one of the Trustees of Smt. Jatnobai Karmchandji Ratanparia Chauhan Charitable Trust.

Vikas P. Jain

Whole-time Director

Mr. Jain spearheads the LawmanPg3 and Integriti brands, alongside supervising Addictions, the lifestyle accessories division. He also manages the retail business of the Company. He is one of the trustees of

Smt. Jatnobai Karmchandji Ratanparia Chauhan Charitable Trust.

Promoters of the company are very experienced and have experience of more than four decades and also the salary taken by the promoters is very nominal salary and despite the increase in profit continuously salary of the promoters remains the same which is very good thing.

Financial Highlights

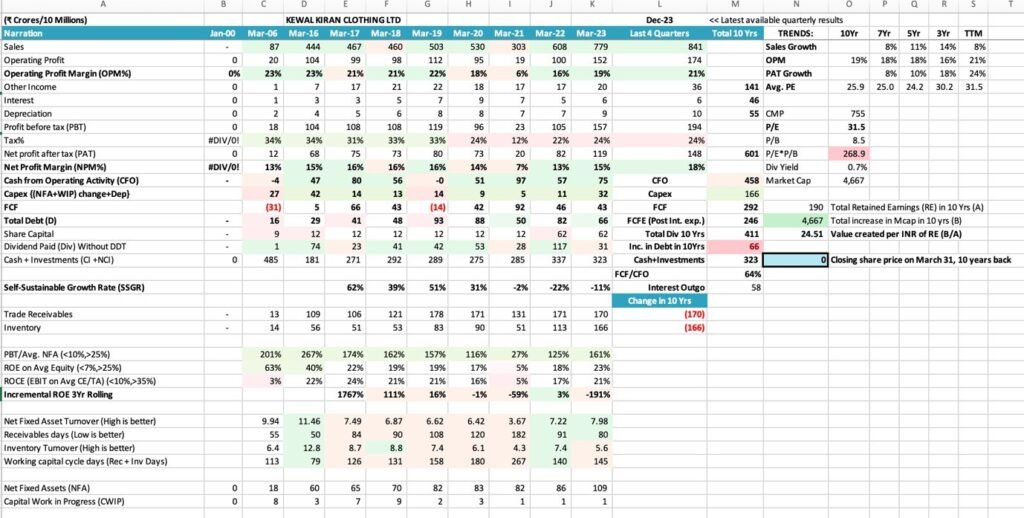

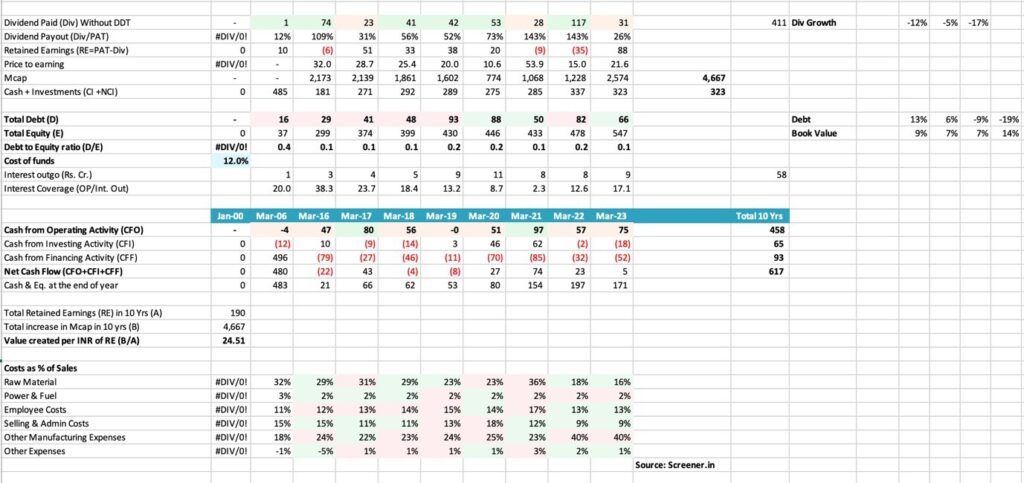

Financials of the company is always good since IPO. When we see the sales growth, it is always in the upper single digit or lower double digit, except during the time of covid sales were down otherwise there is always growth in the number of sales. After the covid we have seen the pace of growth improves and it is between 15 to 20%.

Margins of the company are always stable. If we see the PAT margins, these are always in the range of 13% to 16% of last several years except covid times.

Debt of the company is always manageable, almost since IPO it is net debt free company. Also, except one- or two-year company is always producing positive free cash flow.

Return on Equity (ROE) and Return on Capital Employed (ROCE) of the company is always more than 15% which is a good sign for any company.

The one area of concern which we can say is the stocking of the inventory since past two years otherwise the receivables are also stable from past five years.

Strength of the Company

1. Very Experienced Management – management of the company are very experienced, they have more than four decades experience in this industry. It is because of this management we have not seen losses in any year whether it was the time of 2008 financial crisis or Covid. I have not found any governance issue also of this company.

2. Strong Balance Sheet – very healthy balance sheet with limited debt and always maintain EBITDA margins between 18 to 20%. Almost every year company posted positive cash flows with ROE and ROCE of more than 15%.

3. In-house integrated unit – Company core competency lies in the manufacturing and design skills. Right from designing the apparel to sourcing of raw material to manufacturing of ready-made apparels is carried out in-house. A portion of company production is sold directly though our exclusive stores. This helps it in controlling the inventory and production process. Company believes that this has helped it in achieving optimal capacity utilization and at the same time keeping its costs low which eventually helps it in maintaining healthy margins.

4. Efficient Supply chain management – We procure our raw material from manufacturers and authorized distributors appointed by the manufacturers based on our requirement. We analyze the production requirement on a monthly basis; based on which we place orders to our suppliers. This helps us in minimizing our inventory of raw materials. This also helps us effectively servicing the requirement of our retailer’s, distributor’s and Multi brand outlet.

Weakness of the Company

1. Company operates in very competitive market – Due to this high competition whenever there will be increase in the price of the raw material, company is not able to pass on the price to the customers due to which their margins can be impacted and whenever there is raw material price cool down then they have to give more discount to the customers. In recently held January 2024 concall management talk about this also

2. Company business exhibits seasonality due to the bunching up of festivals like Durga Puja, Diwali, Christmas, etc. in the third quarter of its financial year (October-December quarter), in which historically it has reported higher sales. Any substantial decrease in sales for the October- December quarter could have a material adverse effect on company financial condition and results of operations.

My Viewpoint – Everything looks good for the company whether it is the balance sheet or the quality of the management but there are some points which we should be focused on like the pace of the growth of the sales of the company, if we see the

history of the company the sales growth is always only in the upper single digit, though in last two-year sales growth we have seen in double digit but it is sustained or not I have doubt in this. Though company is looking for inorganic growth also but not able to find any suitable company for acquisition. Second thing is whenever there will be increase in the price of the raw material then company is not able to pass on this increase in price to customers due to high competition. According to me this company is for those investors who wants to look for good fundamentally strong balance sheet with higher single digit growth company.

Leave feedback about this