About the Company

When we read about the promoter’s background then we found that promoter Mr. Mark Saldanha is a part of the family owing Glenmark Pharmaceuticals group. Glenmark was established by his father Gracias Saldanha.

Mr Gracias Saldanha named the company Glenmark after the names of his two sons, Glenn Saldanha and Mark Saldanha (Glenn + mark). Glenn Saldanha is currently the chairman and managing director of Glenmark Pharmaceuticals Ltd. And Mark Saldanha looks after Marksans Pharma Ltd.

In Marksans Pharma, two members of the promoter family are a part of the board of directors, Mr Mark Saldanha and his wife Ms Sandra Saldanha.

Marksans Pharma is engaged in the business of formulation of Pharmaceuticals Products. (Generally we can divide Pharma Industry into two types : API & Formulations. API refers to the key ingredient or chemical that makes the drug work while Formulation is the process in which different chemicals including these key ingredients are mixed in specific ratios to produce a specific drug. Tablets which we purchase from the medical are manufactures by the formulation companies and Marksans Pharma is in this formulation business ). Although marksans earlier said that they want to go in API business only for its internal formulation business (captive consumption) but now step back. However this company till 2010 was in API business also but they sold it as company suffers heavy losses in this segment.

Business Segment

Marksans Pharma operates in both OTC and Rx space (OTC stand for the Over-the-counter, it means one can take medication without prescription from the doctor and Rx means one can take medication only when prescribed by the doctor). Out of total revenues of the company almost 50-50% revenue comes from both the segment but sometimes OTC business contribute 60-65% in total revenue and sometime OTC business contribute 60-70% in total revenue. In FY23, OTC business contributed around 65% in total revenue. Company OTC segment provides good margins as compared to Rx.

Marksans is primarily into exports of oral solid formulations with a special focus around OTC and soft gelatin/hard gelatin formulations.

This company has large presence in US, UK & Europe, Australia & New Zealand and Rest of World (RoW) (UAE, Iraq, Ukraine, CIS, Azerbaijan, Uzbekistan, Sri Lanka, Cambodia and Myanmar). Around 80% of company revenue comes from US and UK. Out of total revenue, 42.6% comes from America, 40.9% comes from UK & Europe, 12.1% comes from Australia & NZ and 4.5% comes from ROW (according to 2022 annual report).

Company manufactures products in the following Therapeutic Segment

- Pain Management : Around 50% of the revenue comes from this therapeutic segment.

- Cough & Cold : this is second most revenue contributor segment after pain management.

- Cardiovascular & Central Nervous System

- Anti-Diabetic

- Gastrointestinal

- Anti-Allergic

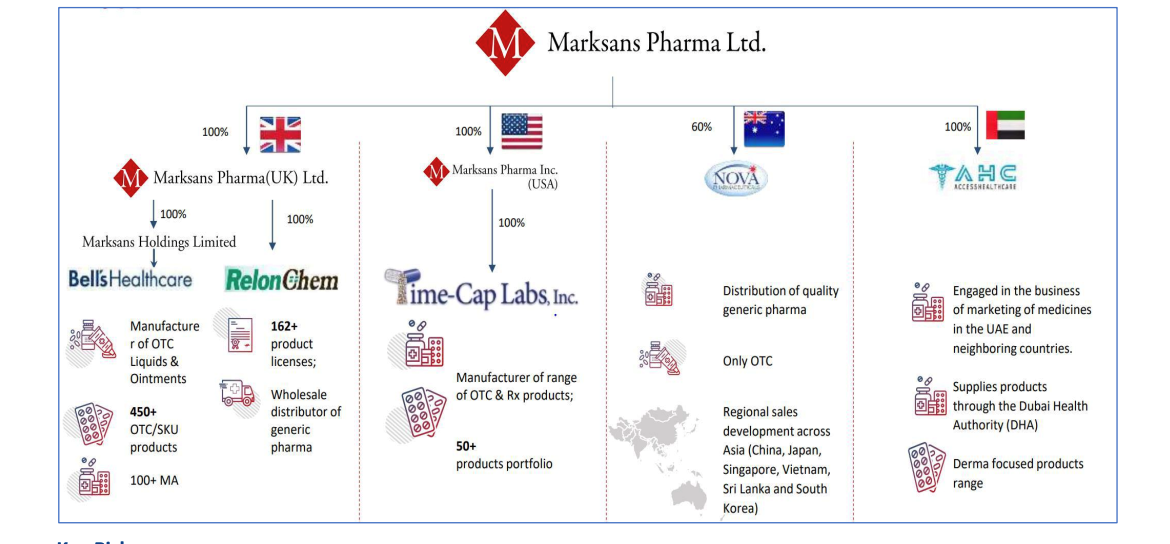

Company Manufacturing Facilities

Reloncham Ltd. (UK Business ) – Wholesale distributor of generic Pharma – Established in 2002; possesses more than 85 product licenses.

Bell’s Healthcare (UK Business )- manufacturer of OTC liquids & ointments – Manufactures and supplies a range of branded and proprietary healthcare pharmaceutical products; coverage of therapeutic areas include cough, cold, pain relief, gastro-intestinal, ear care and skincare for the UK and export markets.

Time-cap (US Business ) – manufacturer of range of OTC & Rx products – Possesses an established tradition of manufacturing pharmaceuticals for over 37 years. Offers over-the-counter products and Rx products. Portfolio comprises more than 30 products.

Nova Pharmaceuticals (Australia & New Zealand Business ) – distribution of quality generic Pharma, only OTC, regional sales development across Asia ( China, Japan, Singapore, Vietnam, Sri Lanka & South Korea ) – A dynamic Australia-based (headquartered in Sydney) pharmaceutical company providing value to customers by delivering quality affordable medicines. Engages in regional sales, marketing and business development across Asia (China, Japan, Singapore, Vietnam, Sri Lanka and South Korea).

AHC (UAE Business) : Source: August 2022 Concall

Note: On Oct 11, 2022, Marksans entered into a Business Transfer Agreement with Tevapharm India Private Limited, to acquire its business relating to the manufacture and supply of bulk pharmaceutical formulations in Verna, Goa, as a going concern on a slump sale basis. Through the acquisition, the company plans to double the existing Indian capacity from 8 billion units per annum currently. Company plans to acquire marketing licenses in Europe and USA to expand business operations in regulated markets. (source : November 2022 Concall transcript )

End Consumers of Company :

- Retail Chains

- Pharmacy Stores

- Hospitals

- Institutions

Financials of the Company

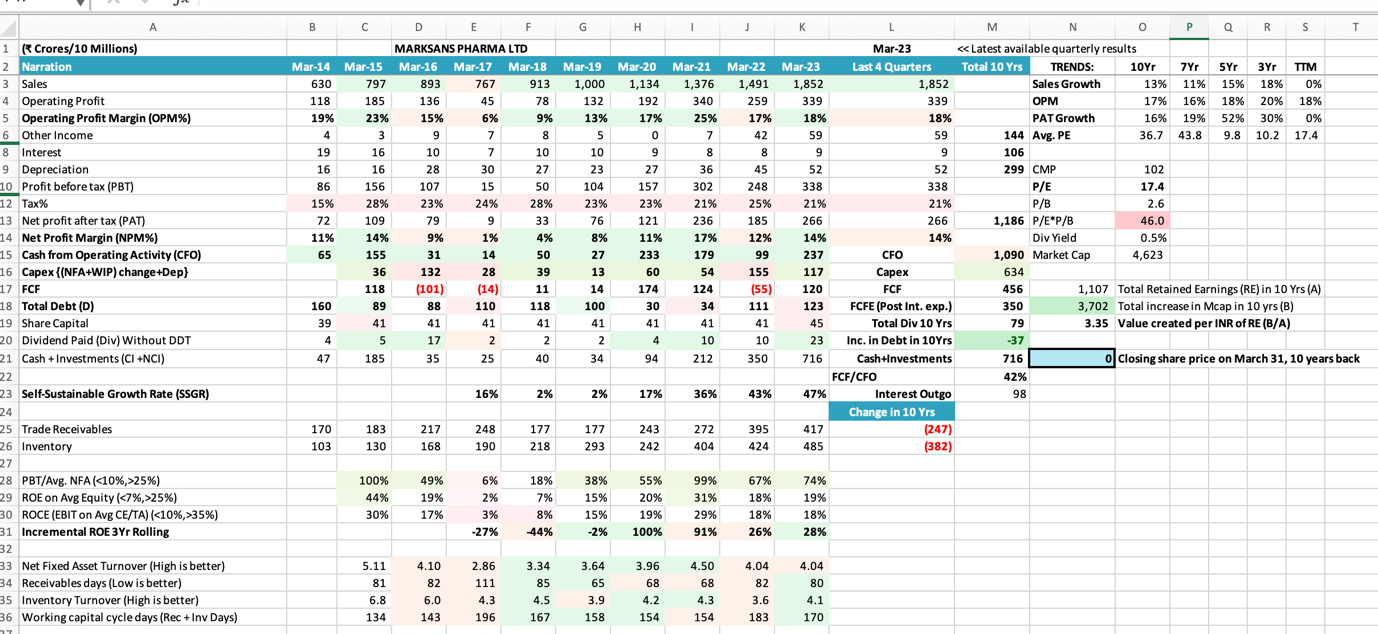

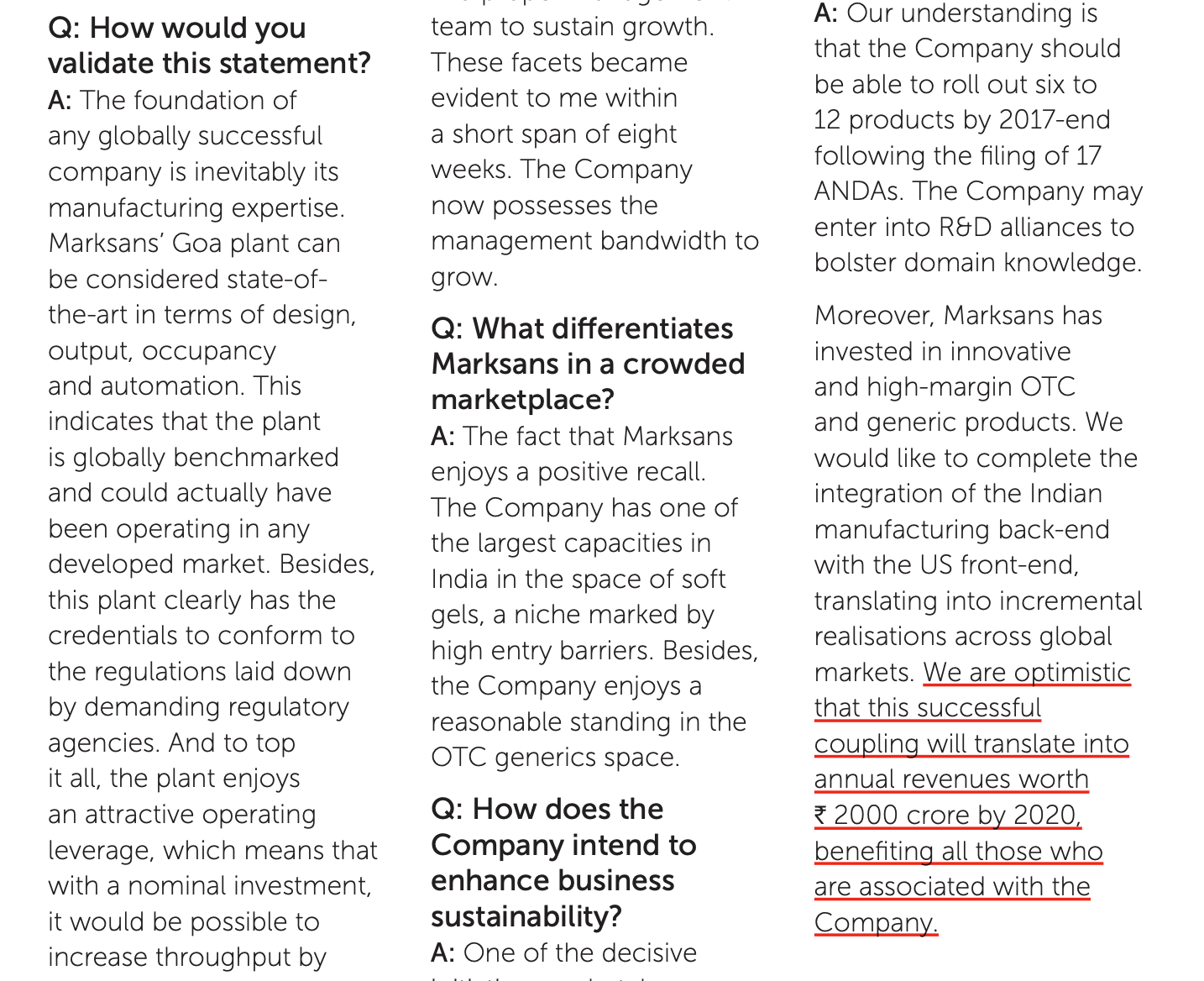

So as we have seen that sales of the company is growing at a pace of 13% YoY from 630 crore in FY2014 to 1852 crore in FY2023. In 2016 Annual report management said that they will get 2000 crore annual revenue by FY2020 and as we have seen that till FY2023 company still not achieve that target.

(Source – Marksans Pharma Annual Report 2016)

We have seen that after 2018 company financials are growing in a good way as OPM is growing from 9% to 17% and management expects it will be around 17 to 20% continuously but before 2018 financials are fluctuating a bit.

Before 2018 PAT is also not consistent but after 2018 PAT of the company is continuously growing except 2022. PAT is growing 16% YoY in last 10 year.

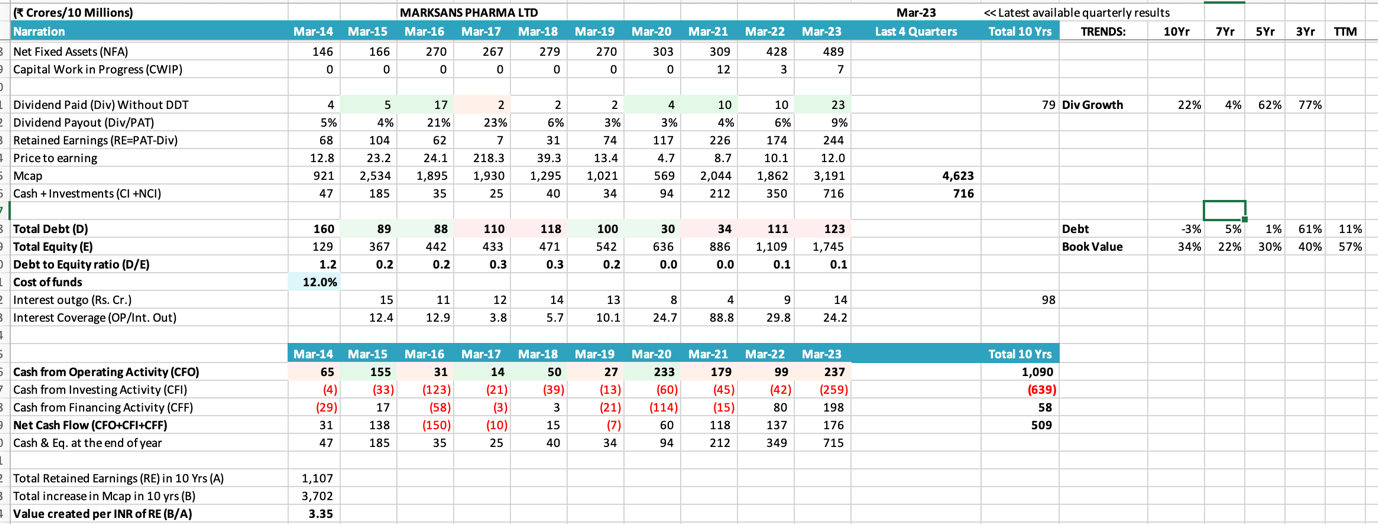

Company has positive Free Cash flow after 2018 except 2022 but before 2018 company had hardly any free cash flow, as of now company is sitting at 716 crore cash & cash equivalents, means if company wants any acquisition, then it can easily do so without needed any cash from outside.

Company is almost debt free having no long-term debt from past three years. Now company is almost debt free but if we saw the history of the company during the period of 2005 to 2014, this company was not able to repay the debt and at one point around 2011 becomes bankrupt and at one point company faces the situation that they sold the API business and its Mumbai offices premises also and still not able to repay the debt and due to this company entire net worth was wipe out and it becomes a sick company.

Trade Receivables of the company is increased from 170 crores in FY2014 to 417 crores in FY2023, which is not good as it signifies that company has lot of cash stuck in market and it requires fund from outside for its day-to-day operations, but management said that since sales is increasing so the trade receivable amount is also increasing.

Inventory of the company is also increases from 103 crore in FY2014 to 485 crore in FY2023 which is also not good and management is giving same reason which I mentioned above.

Company ROE & ROCE is currently around 17 to 18% which is okay, but when we saw ROE & ROCE of last 10 years then we can find that these ratios are fluctuating a lot which is not a good thing.

Net Fixed Asset Turnover – NFAT (it means how efficiently any company is using its assets to convert into sales), this ratio is almost stable for this company except during 2017 when it was down and that is because of delay of integration of company’s newly acquired US company Time Cap Labs

Company receivable days are also stable which is around 80 days when we saw from FY2014 to FY2023.

When we check the inventory turnover ratio of the company, we find that it is continuously in downtrend from 6.8 in FY15 to 4.1 in FY23 which is not a good sign in management of the inventory. A decline in the inventory turnover ratio indicates that the efficiency of utilization of inventory by the company is coming down over the years. It means that the company is using comparatively more inventory to run its business. However management explained this in the February 2021 concall

Strengths of the Company

- Financials are improving: – if we see from 2018 onwards, we find that company financials are improving a lot, now from past two years company’s long term debt is almost zero, revenue of the company is increasing at a good rate and I think it will achieve their dream target of 2000 crore sales in FY24 which they spoke about since 2015, now company margins are also stable, so in every parameters we can see that financials are good now.

- Positive Free cash flow: – since 2018 company, every year company is making free cash flow every year which is a good sign as it is the free cash flow which is actually coming in the hands of the company.

- Company is sitting on more than 700 crore cash: – since company has enough cash and we know that this company is always looking for inorganic growth, so I think they have enough cash in hand to go for inorganic growth without needed any cash from outside.

- Product mix is continuously increasing: – if the company want to grow they need to increase their product mix, only then it will grow, which is they are doing continuously which is a good sign.

- Company has differentiated position in the US & UK market on Softgel capsules.

- Company is continuously increasing the manufacturing capacity, recently they acquired one more manufacturing facility Teva in Goa to double their capacity. It shows that management see growth in near future and that is why they continuously increasing their capacity.

Valuation of the company

Company is trading at a price multiple of 17 and having market cap to sales of 2.5 which is okay according to me.

My Viewpoint

Though the company financials are improving a lot since 2018 and company is debt free from past three years and it is sitting at cash of more than 700 crores which means they can go for inorganic growth without need of fund from outside and future prospects of the company is also looking good but I will not be going to invest in this company due to multiple reasons which is mentioned below.

- Never fulfill the guidance provided on time: – I have observed number of times that whatever guidance they gave to shareholders; they never fulfill that on time. In 2015 they said that they will reached at revenue of 2000 crore till 2020 but still in 2023 they have not reached at this level. In 2015 company acquired one US company Times Cap and management said that they will integrate this newly acquired business with its company within a year but they took almost three years to complete integration of this newly acquired company. When we read the 2016 annual report, management said that they will create R&D centre in Navi Mumbai and complete this in one year, but it also delayed by two years.

- Overstating of profits and non-provisions for the foreign exchange losses on FCCBs by Marksans Pharma Ltd.: – when we read the annual reports of 2008 onwards we find that auditor of the company repeatedly highlighted in its reports that profits of the company were overstated significantly as it did not provide for the foreign exchange losses on FCCBs in its reported financials, even though as per the companies act it should have done so. Like in 2009 annual report auditor highlighted that profit of the company are overstated by 53 crore

No Provision have been made during the year for Rs.5335 lacs towards Foreign Exchange Difference account in case of Foreign Currency Convertible Bond. The Management is of the opinion the determination and Crystallisation of Liabilities is dependent upon the outcome of uncertain future events or actions not wholly within the control of the Company and therefore, the same has been considered as ‘Contingent Liability’ as on 31.3.2009 and to that extent profit for the year ended 31.3.2009 is overstated.

Since this is clearly according to me an issue of corporate governance and if company is of such mindset then anytime in the future they can do the same if needed. I always prefer to stay away from such companies which have corporate governance issue.

- Plans for manufacturing plant at Nagpur by Marksans Pharma Ltd: – When I read the concall transcript we come to know after a gap of almost 5 years that company got an allotment of 10 acres of land in Nagpur for manufacturing plant

- It seems that company is doing some manipulation on Intangible assets: – When we read the 2012 annual report, we find that company impaired its intangible assets by almost 80% when it reduced their value from 137 crore in 2011 to 27 crore in 2012, a decline of about 110 crore. However management explained the same but it does not fit according to me The expenses incurred on development of process/product and compliance with regulatory procedures of US FDA and other global health authorities in filing of Abbreviated New Drug Application (ANDA), Market Authorisation/Site Variation Licenses for CRAMS and MHRA procedure for Market Authorisation/Site Variation Licenses are capitalised and identified as intangible assets, the carrying value of the Intangible Assets have been reduced to their recoverable amount in the Balance Sheet as on 31 March 2012…The recoverable amount is as per the binding out licensing/distribution agreements for the respective products.

And again in 2019 annual report we find that it has disposed off the goodwill of about 27 crore.

- No spending in CSR activities in many years despite having profit: – Now from last three years company is spending in CSR activities but before that despite profit incurred company has not spend anything in CSR and every time they gave reason that they have not find suitable for which they can spend CSR amount which according to me does not fit.

These are some of the points because of which I don’t want to invest in this company as I am always looking for invest for long time like more than 8 years and if company did anything like this then it may affect the return also.

Leave feedback about this